Featured

How banks protect a deceased depositor's bank account and their rightful heirs

As a rule of thumb, only joint accountholders, legal heirs, or executors/administrators of estates can access a deceased depositor’s account.

Important Reminders:

- It is the bank’s obligation to safeguard the security and integrity of its depositors’ accounts and transactions.

- In the case of deceased depositors, banks deal with the rightful heirs (or the appointed executor or administrator of the estate) regarding the details of the accounts and the remaining funds.

Losing a loved one is never easy, and banks understand how difficult and overwhelming this time can be for those who are left behind. Beyond the emotional toll, families are often faced with financial matters that need to be addressed.

As a bank trusted by our depositors, Metrobank prioritizes the protection of its depositors’ accounts – including those of our deceased accountholders. Metrobank has, after all, promised that our depositors are in good hands. We are likewise mandated to do so by various banking laws and regulations that require financial institutions to safeguard depositors’ accounts.

This protection remains in place even after a depositor passes away. Note that Metrobank, like any other bank, has no vested interest in keeping its deceased depositors' money. As we sympathize with the grieving family, we do our part in making sure that only the rightful parties can access the deceased depositor’s bank account and funds. As such, in releasing any transaction information, and more so the funds from a deceased depositor's account, we ensure that we are dealing with all rightful heirs, and that such disclosure or release has their collective consent or approval.

If no proof of consent can be provided or if there is any conflict or dispute among said heirs, the bank takes a neutral stand and will not release any information to any one party or heir. Metrobank believes that our courts are the proper venue and authority to determine the rights of and to settle any issue among disputing heirs.

Here's a quick guide on how Metrobank handles accounts of its deceased depositors:

What happens to bank accounts when someone passes away?

We follow strict rules and processes to ensure the protection of a deceased depositor's account from unauthorized access.

As soon as the bank is informed/receives information regarding the death of a depositor, his/her accounts are put on hold.

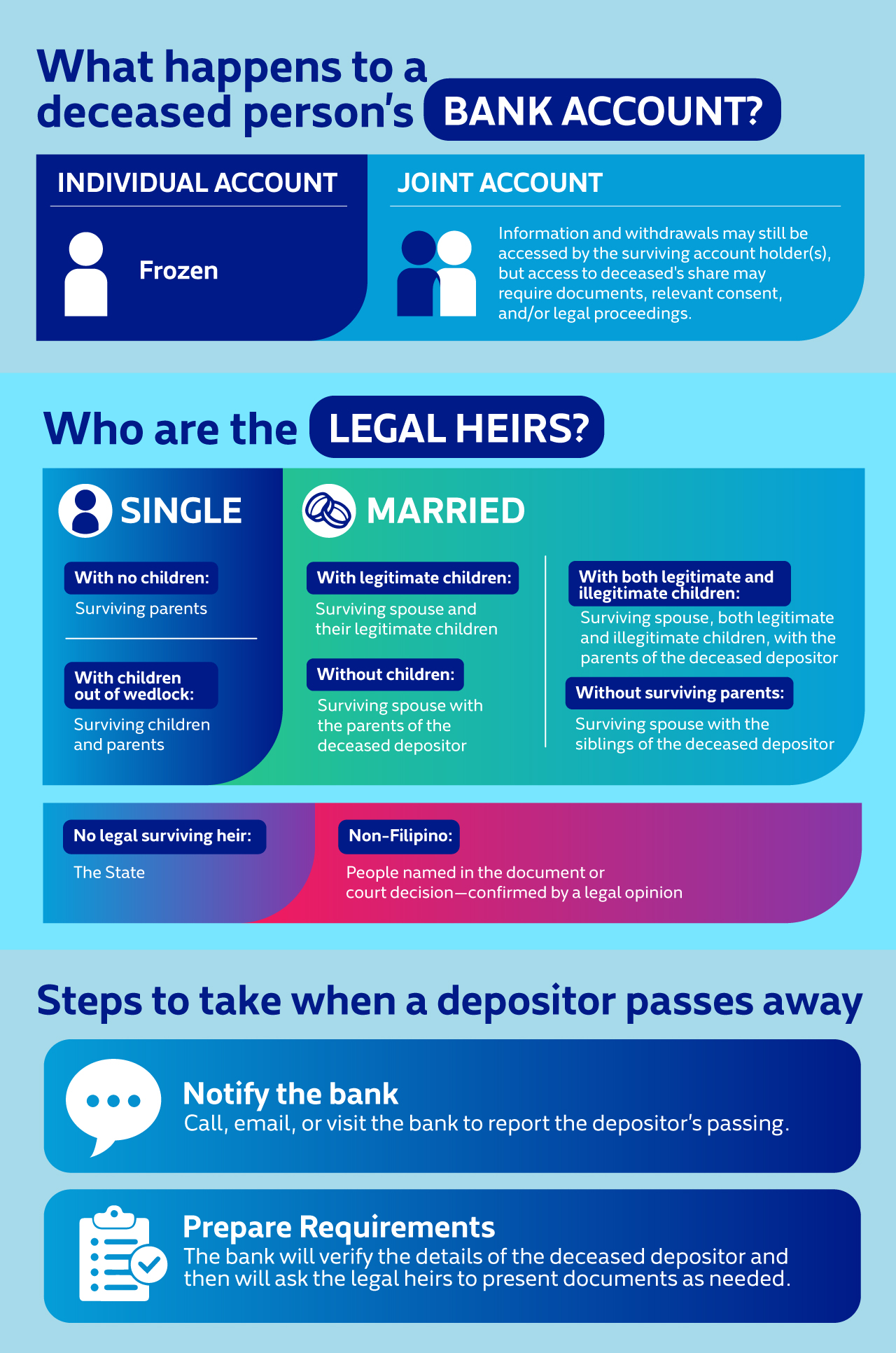

Individual vs. Joint Accounts

- Individual accounts (solely owned by the deceased) are put on hold.

- Joint accounts (shared by two or more people) – surviving account holder(s) may access as to his share, but release of the deceased depositor’s share may require submission of requirements or legal proceedings.

Who can claim the funds?

The legal heirs of a deceased depositor depend on his/her family situation. Typically, for married depositors with children, the surviving wife or husband and the children are the rightful heirs to a deceased depositor's account.

For example:

A is married to B, and together they have three children: X, Y, and Z.

B is a depositor and maintained an individual account, as well as a joint account with each of his three (3) children.

B died, and her family now make a claim on the bank.

- Under the law, B’s heirs (A, X, Y, and Z) have equal rights to B's bank account.

- B’s heirs can request for the account balances on the accounts maintained by B with Metrobank, for purposes of settling her estate.

- Even if requested by A, a legal heir, Metrobank can only disclose B’s co-depositors only if they consent to such disclosure.

- Even if requested by A, a legal heir, Metrobank can only disclose account and transaction history prior to death only upon the written consent of all the other heirs (X, Y, and Z). Otherwise, A will need to obtain a court order to instruct Metrobank to release the information regarding the accounts maintained by B.

This illustrates the power of Republic Act 1405 or the Bank Secrecy Law, which prohibits any person from unauthorized access to a bank account-even that of deceased depositors. Simply put, no one can just go to your bank and inquire about your accounts and banking transactions.

Here are more details on how we determine a deceased depositor’s heirs, based on different family situations:

A. Single depositors with no children – The legal heirs are the surviving parents. If there are no parents, the deceased depositor’s siblings can claim. If no surviving siblings, nephews and nieces may claim.

B. Single depositors with children out of wedlock – The surviving parents and children can claim the funds.

C. Married with legitimate children – The surviving spouse and legitimate children are entitled to the funds.

D. Married with legitimate and illegitimate children – The surviving spouse and both the legitimate and illegitimate children can claim.

E. Married, no children, no surviving parents – The surviving spouse and deceased’s siblings can claim.

F. No surviving legal heirs – If there are no legal heirs, the funds will go to the state.

G. Non-Filipino depositor – The rightful claimants must be identified based on legal documents verified by legal counsel.

Steps to take when a depositor passes away

-

Notify the bank – Call, email, or visit the bank to report the depositor’s passing.

-

Bank verification – The bank will confirm the deceased’s nationality, check if a will exists, verify claimants’ identities and relationships, and assess any outstanding debts.

-

Submit required documents – Commonly needed documents include:

- Certified true copy of the death certificate

- Proof of relationship with the deceased (e.g., birth or marriage certificates)

- Court orders (if applicable)

- Additional requirements depending on how estate is settled

- It’s best to check with the bank’s branch officers or relationship manager for a full list of required documents.

-

Understand taxes and legal obligations – The deceased depositor’s balance may be subject to taxes and legal processes. Bank officers can guide heirs on how to comply with these requirements.

-

Resolve disputes properly – In cases of conflicting claims, the bank may advise claimants to settle disputes through legal proceedings. Under the Bank Secrecy Law, banks cannot disclose account details without proper authorization.

Planning ahead: Securing your family’s future

Being proactive can prevent difficulties in accessing a deceased loved one’s assets.

Consider:

- Writing a will to clearly state how assets should be distributed

- Setting up a living trust to ensure smooth asset transfer

- Consulting financial experts, such as your bank’s wealth management team, to plan effectively

While death is never easy to talk about, preparing for it can make a significant difference for your loved ones. Starting the conversation today can help protect your family from unnecessary financial stress in the future.

More Smart Reads

Turning “someday” into “now” for your family’s next big purchase with Goals Made Real

Feb 20, 2026

The Love Language of Money: How your shared financial habits can say ‘I Love You’

Feb 12, 2026

Private Wealth investors shift to disciplined, opportunity-driven asset allocation in 2026

Feb 11, 2026